L-Istatistika Strutturali tan-Negozju: 2024

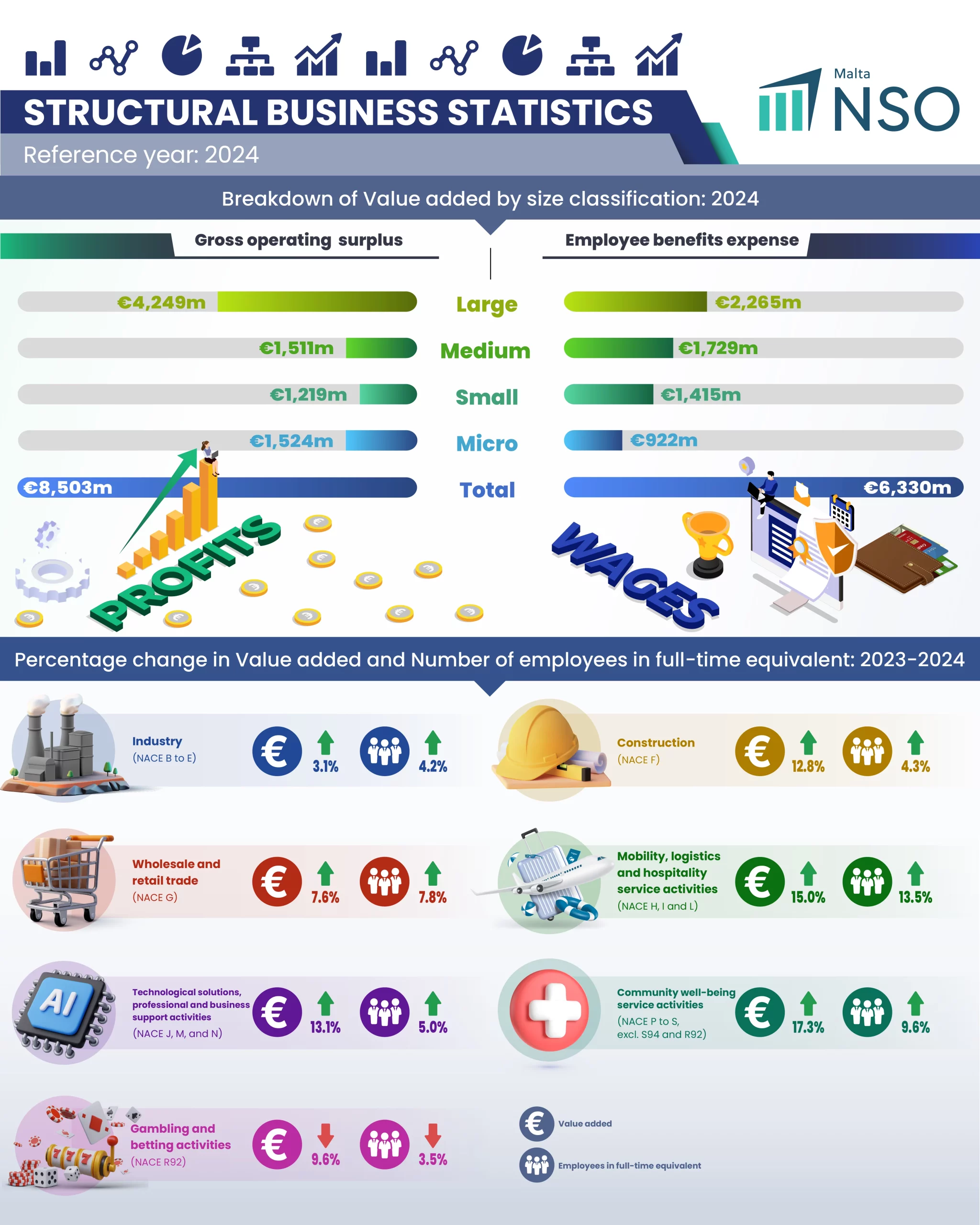

Fl-2024, l-ekonomija kummerċjali mhux finanzjarja f’Malta li tinkorpora fiha l-attivitajiet kollha tas-suq ikklassifikati fit-Taqsimiet tan-NACE minn B sa S (barra Taqsimiet tan-NACE K, O u Diviżjoni S94) iġġenerat mal-€14.8-il biljun f’Valur miżjud, li jiġu daqs żieda taʼ 9.2 fil-mija fuq is-sena taʼ qabel. Dan kien magħmul minn €8.5 biljuni fi Qligħ operattiv gross (jew profitti) u minn €6.3 biljuni fi Spejjeż tal-benefiċċji tal-impjegati. L-għadd relattivament żgħir taʼ intrapriżi kbar ikkontribwixxa għall-akbar sehem taʼ Fatturat nett, Valur tal-output u Investimenti grossi f’assi tanġibbli mhux kurrenti. Il-Qligħ operattiv gross kien maqsum b’mod indaqs bejn l-SMEs u l-intrapriżi kbar. L-SMEs irreġistraw żieda taʼ 14.5 fil-mija fil-Valur miżjud meta mqabblin mal-2023. Fost l-SMEs, l-akbar żieda fil-Valur miżjud dehret fl-intrapriżi ta’ daqs medju, bi 19.5 fil-mija (Tabelli nri 1 u 2, Ċart nru 1).

Il-qofol tal-attività fl-oqsma

L-akbar tkabbir fil-Fatturat nett kien irreġistrat fil-qasam tal-Kummerċ bl-Ingrossa u bl-Imnut (€1.9 biljun). Wara dawn, kien hemm il-qasam tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju (€1.8 biljun) u l-Attivitajiet ta’ servizzi ta’ mobbiltà, loġistika u ospitalità (€1.5 biljun). Il-qasam tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju kellu l-akbar tkabbir fʼtermini taʼ negozji, bʼżieda taʼ 1,163 negozju. Huwa ħaddem 2,566 ħaddiem aktar u ħallas €231.1 miljun aktar fi Spejjeż tal-benefiċċji tal-impjegati meta mqabbel mal-2023. Dan il-qasam irreġistra l-ikbar tnaqqis miż-żewġ oqsma li rreġistraw tnaqqis fʼInvestimenti grossi f’assi tanġibbli mhux kurrenti tal-Attivitajiet, tnaqqis minn €209.9 miljun fl-2023 għal €164.4 miljun fl-2024, filwaqt li l-qasam tal-Logħob tal-azzard u tal-imħatri rreġistra biss tnaqqisa żgħira. Fl-2024, il-qasam tal-Attivitajiet tal-Benessri tal-komunità kkontribwixxa l-akbar żieda fil-Valur miżjud, bi 17.3 fil-mija fuq l-2024 (Tabella nru 4).

Il-ħidma tal-intrapriżi kbar

Fl-2024 l-intrapriżi kbar żdiedu bi tlieta, ħaddmu 2,456 ħaddiem aktar u ħallsu €161.2 miljun aktar fi Spejjeż tal-benefiċċji tal-impjegati meta mqabblin mas-sena taʼ qabel. Il-Valur miżjud tagħhom żdied bi 3.1 fil-mija, meta mqabbel maż-żieda taʼ 14.5 fil-mija rreġistrat mill-SMEs (Tabella nru 2).

Il-ħidma taʼ intrapriżi żgħar bʼkapitalizzazzjoni medja (SMCs)

Fl-2024, l-intrapriżi kklassifikati bħala intrapriżi żgħar bʼkapitalizzazzjoni medja (SMCs) irreġistraw €1.4 biljun fʼValur miżjud jew 9.4 fil-mija tat-total għall-ekonomija kummerċjali mhux finanzjarja. Dan huwa tnaqqis żgħir mis-sehem tal-Valur miżjud fl-2023 (10.4 fil-mija). L-intrapriżi SMCs irreġistraw tnaqqis fil-varjabbli ewlenin kollha barra mill-Fatturat nett, il-Valur tal-output u l-Ispejjeż tal-benefiċċji tal-impjegati, li żdiedu bi 3.7 fil-mija, bi 3.1 fil-mija u bi 2.7 fil-mija, rispettivament. L-intrapriżi SMCs kienu qegħdin fis-sebgħa oqsma taʼ attività, bl-aktar preżenza qawwija tagħhom tkun fil-qasam tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju, bʼ25 negozju u 9,555 ħaddiem. Madankollu, l-intrapriżi SMCs fil-qasam tal-Attivitajiet ta’ servizzi ta’ mobbiltà, loġistika u ospitalità rreġistraw l-akbar Fatturat nett, Valur tal-output u Valur miżjud bʼ€798.6 miljun, bi €827.5 miljun u bʼ€436.3 miljun rispettivament (Tabella nru 3).

Indikaturi ewlenin fl-oqsma tal-attività bil-klassi tad-daqs

Matul l-2024, fost l-erba’ livelli tal-klassifikazzjoni tad-daqs, l-akbar għadd ta’ intrapriżi attivi kienu l-mikrointrapriżi fis-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju; fl-Attivitajiet ta’ servizzi ta’ mobbiltà, loġistika u ospitalità; u fl-Attivitajiet ta’ servizzi tal-benesseri tal-komunità, bi 15,235, bi 11,138 u b’9,590 negozju rispettivament. Il-Fatturat nett kien ġej l-aktar minn intrapriżi kbar fil-qasam tal-Attivitajiet tal-logħob tal-azzard u tal-imħatri, li wasslu għall-akbar ammont taʼ Valur tal-output iġġenerat. Intrapriżi kbar fil-qasam tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju rreġistraw l-akbar ammont taʼ Valur miżjud u Qligħ operattiv gross. L-akbar spiża taʼ pagi, ekwivalenti għal 9.4 fil-mija tat-total fl-oqsma kollha, kienet imħallsa minn intrapriżi medji tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju (€597.0 miljun). Dawn l-intrapriżi ma ħaddmux l-akbar ammont ta’ impjegati, peress li l-akbar għadd ta’ impjegati kienu impjegati ma’ intrapriżi ta’ daqs kbir fi ħdan l-istess qasam (19,196). L-akbar ammont taʼ Investimenti grossi f’assi tanġibbli mhux kurrenti kien irreġistrat minn intrapriżi kbar fl-Attivitajiet ta’ servizzi ta’ mobbiltà, loġistika u ospitalità (€1.2 biljun) (Tabella nru 5, Ċart nru 3). L-Industrija, l-oqsma tal-Attivitajiet ta’ servizzi tal-benessri tal-komunità u tal-Kummerċ bl-ingrossa u bl-imnut kellhom l-akbar sehem fl-Ispejjeż tal-benefiċċji tal-impjegati mill-Valur miżjud, filwaqt li l-akbar sehem tal-oqsma l-oħra fil-Valur miżjud kien il-Qligħ operattiv gross (Ċart nru 2).

Nota: Din iċ-ċart ma turix il-valuri negattivi fuq l-assi orizzonali. Perċentwal żgħir ta’ intrapriżi taʼ daqs mikro fi ħdan il-qasam tal-Attivitajiet tal-logħob tal-azzard u tal-imħatri wrew valuri negattivi u għalhekk mhux qed jintwera fiċ-ċart.

Il-kontribut tal-SMEs għall-Valur miżjud

Meta mqabblin mal-intrapriżi kbar, l-SMEs kellhom sehem ogħla taʼ Valur miżjud fl-oqsma kollha ħlief għall-Industrija u l-Attivitajiet tal-logħob tal-azzard u tal-imħatri. L-SMEs kienu dominanti l-aktar fil-qasam tal-Kostruzzjoni, bis-sehem tagħhom jilħaq is-86.4 fil-mija tal-Valur miżjud iġġenerat minn dan il-qasam (Tabella nru 5, Ċart nru 3). Is-sehem tal-Qligħ operattiv gross mill-Valur miżjud kien ogħla għall-intrapriżi kbar u mikro, filwaqt li sehem l-Ispejjeż tal-benefiċċji tal-impjegati kien akbar f’intrapriżi medji u żgħar (Ċart nru 4).

L-għamla legali tal-intrapriżi

Is-sidien li jaħdmu għal rashom u s-sħubiji rreġistraw l-akbar għadd ta’ negozji b’75.2 fil-mija tat-total, filwaqt li l-intrapriżi bʼresponsabbiltà limitata ħaddmu l-akbar għadd taʼ ħaddiema b’86.5 fil-mija tat-total. Fl-2024, l-intrapriżi b’responsabbiltà limitata ġġeneraw 88.1 fil-mija tal-Valur miżjud (Tabella nru 6).

Industriji relatati mat-turiżmu

Fl-2024, l-intrapriżi fʼindustriji relatati mat-turiżmu żdiedu bʼ497 negozju u bʼ4,001 ħaddiem. Huma rreġistraw Fatturat nett taʼ €9.0 biljuni u Valur miżjud taʼ €1.9 biljun (Tabella nru 7).

Il-karatteristiċi tan-negozju bil-lokalità

Fl-2024, l-intrapriżi b’indirizz irreġistrat f’Birkirkara, San Ġiljan u Ħal Luqa ġġeneraw l-akbar ammonti taʼ Valur miżjud fl-ekonomija mhux finanzjarja Maltija (Mappa nru 1). L-Investimenti grossi f’assi tanġibbli mhux kurrenti kienu l-ogħla f’Ħal Luqa, San Ġiljan u l-Belt Valletta (Mappa nru 2).

Mappa nru 1. Il-Valur miżjud bl-indirizz irreġistrat (LAU2)

Nota: Il-wisaʼ meħud minn intrapriżi kbar qiegħed ikun allokat lill-indirizz irreġistrat rispettiv tagħhom, minkejja li dawn l-intrapriżi jistgħu jkunu joperaw minn friegħi fʼlokalitajiet differenti.

Mappa nru 2. L-Investiment gross f’assi tanġibbli mhux kurrenti aggregat, bil-lokalità tal-indirizz irreġistrat (LAU2)

Nota: Il-wisaʼ meħud minn intrapriżi kbar qiegħed ikun allokat lill-indirizz irreġistrat rispettiv tagħhom, minkejja li dawn l-intrapriżi jistgħu jkunu joperaw minn friegħi fʼlokalitajiet differenti.

Tables

Tables

The SME classification used in this news release is organised according to the staff headcount and the ‘Turnover’ financial ceilings recognised in annex article 2 of Commission Recommendation 2003/361/EC.

Methodological Notes

1. The SME classification used in this news release is organised according to the staff headcount and the ‘Net turnover’ financial ceilings recognised in annex article 2 of Commission Recommendation 2003/361/EC.

2. The main variables referred to in this news release, for both 2023 and 2024, refer to statistical units as compiled and transmitted to Eurostat at statistical unit ‘Enterprise’ level. This is in accordance with Council Regulation (EEC) No 696/93.

During the consolidation of enterprises for statistical purposes units classified under NACE Rev. 2 division 64.20 (Activities of holding companies) that provide services to the enterprises they are a part of are considered part of the non-financial business economy and as such are not treated as part of the financial population.

3. Structural Business Statistics (SBS) aim to provide a cross-sectional view of the business economy based on the structure, performance and behaviour of the industries. Presented according to the activity classification, they cover industry, construction, trade and services production of businesses within the Maltese territory. These statistics can be broken down by activity and employment size class levels.

4. For reference year 2024, around 6,280 business units were selected and contacted. A sample was used to cover industries in the non-financial business economy. For larger companies, a census survey was targeted. The questionnaire asked for details related to the performance of the enterprise during the financial year under review. The information collected was supplemented and supported by additional information extracted from administrative data sources. The data was grossed up to represent the total non-financial business population active during the year.

5. The domain activity names used in this news release are not internationally recognised but were established internally taking into account the respective domestic industry categories, national exigencies and the users’ needs.

6. The business activities covered by SBS are defined under the European Business Statistics (EBS) regulation (EU) 2019/2152. The SBS survey covers NACE Sections B to N and P to S, excluding S94. Activities classified under Section K (Financial and insurance activities, NACE 64–66) are not included in this news release. Sections A (Agriculture and Fisheries) and O (Public administration) are also excluded.

7. SBS data is not fully comparable with data produced by National Accounts due to some conceptual and methodological differences. These include adjustments made in National Accounts for production activities not captured in enterprise reporting, such as estimates related to informal economy transactions, as well as methodological concepts such as Financial Intermediation Services Indirectly Measured (FISIM). SBS data is unadjusted and reflects the official values reported by active resident enterprises operating in the non-financial business economy of Malta, based on data as reported by businesses.

8. Definitions (based on the Commission Implementing Regulation (EU) 2020/1197):

● Net turnover includes total sales and other operating income and is expressed net of VAT.

● Value of output measures the amount actually produced, based on sales, including changes in stocks and neutralising the impact of goods resold in the same condition as purchased.

● Value added represents the value a business adds through its production process. It reflects the net contribution of a business to the economy and is equivalent to the combined Gross operating surplus and Employee benefits expense.

● Gross operating surplus is the surplus generated by operating activities after the labour factor input has been recompensed. It can be calculated from the Gross value added less the Employee benefits expenses. Simply put, Gross operating surplus is a measure of profitability before accounting for interest, income taxes, depreciation, amortisation, revaluations, provisions and other non-operating expenses.

● Employee benefits expense is defined as the total remuneration, in cash or in kind, payable by an employer to an employee (regular and temporary employees as well as home workers) in return for work done by the latter during the reference period. Employee benefits expenses also include taxes and employees’ social security contributions retained by the unit as well as the employer’s compulsory and voluntary social contributions.

● Gross investment in tangible non-current assets is defined as investment during the reference period in all tangible goods. Included are new and existing tangible capital goods, whether bought from third parties or produced for own use (i.e. capitalised production of tangible capital goods), having a useful life of more than one year including non-produced tangible goods such as land. Investments in intangible and financial assets are excluded.

● Persons employed are people engaged in productive activities in an economy. The concept includes both employees and self-employed (i.e. inclusive of working proprietors, partners and unpaid family workers). The latter category may include persons who do not receive compensation in the form of wages, salaries, fees, gratuities, piecework pay or remuneration in kind. The name used for this variable by Eurostat in the Database is Number of employees and self-employed persons.

● Number of employees is defined as those persons who work for an employer through a contract of employment and receive compensation in the form of wages, salaries, fees, gratuities, piecework pay or remuneration in kind.

● Number of employees in full-time equivalent units is a unit of measure which transforms the number of employees in a way which makes employees working a different number of hours per week comparable. This conversion is mainly relevant to part-time workers. The unit is obtained by comparing an employee’s average number of hours worked to the average number of hours of a full-time worker. A full-time person is therefore counted as one FTE, while a part-time worker gets a score in proportion to the hours he or she works. For example, a part-time worker employed for 20 hours a week where full-time work consists of 40 hours, is counted as 0.5 in FTE.

9. SBS data in this news release was classified according to the SME classification in the Commission Recommendation 2003/361/EC “definition of micro, small and medium-sized enterprises adopted by the Commission”. The ceilings of this classification were applied to Net turnover and employment only (both criteria must be met by individual statistical units). The balance sheet total ceiling was not applied as such information is not available for statistical units involving self-employed. Users of this news release must appreciate that there is not a single definition of what a SME is. Other SME definitions may be used by other institutions, authors and publications. For instance, Eurostat defines SMEs solely based on the employment within an enterprise.

| Company category | Staff headcount | Net turnover | |

|---|---|---|---|

| Medium | <250 | ≤ €50m | |

| Small | <50 | ≤ €10m | |

| Micro | <10 | ≤ €2m |

Companies that do not fall within these categories, i.e. either with employment more than 249 or with Net turnover greater than €50 million, are considered as Large.

Similarly, there are also different definitions of Small Mid-Cap (SMC) enterprises. For the purposes of this release, SMCs are defined in line with the European Commission Recommendation on the definition of small mid-caps enterprises adopted in July 2025, as enterprises with employment between 250–750 and Net turnover not exceeding €150 million. This definition differs from the SMC definition used in the 2023 News release.

10. Enterprises may change their classification from one year to the other if significant changes occur in their respective NACE, employment or turnover.

11. Tourism related industries in this news release were classified according to the list drawn up by the UN Tourism (formerly known as UNWTO) International Recommendations for Tourism Statistics 2008. Firm-level data cannot distinguish between consumption by visitors and non-visitors and for this reason, the industries exposed to tourism demand are identified and aggregated together. This aggregate does not represent the ‘tourism industry’ but simply sums the main variables of all establishments belonging to the list of tourism related industries, regardless of whether all their output is provided to visitors and of the degree of specialisation of their production process. This aggregate also leaves out other consumption expenditure components by visitors from other non-tourism related industries. The sub-category ‘mainly tourism’ is a sub-category established in the same UN Tourism (formerly known as UNWTO) manual to identify the most intensively exposed industries to tourism demand. The NACE industries that are considered as tourism related and ‘mainly tourism’ are listed below:

H4910 Passenger rail transport, interurban.

H4932 Taxi operation.

H4939 Other passenger land transport n.e.c.

H5010 Sea and coastal passenger water transport.

H5030 Inland passenger water transport.

H5110 Passenger air transport, also ‘mainly tourism’.

I5510 Hotels and similar accommodation, also ‘mainly tourism’.

I5520 Holiday and other short-stay accommodation, also ‘mainly tourism’.

I5530 Camping grounds, recreational vehicle parks and trailer parks, also ‘mainly tourism’.

I5610 Restaurants and mobile food service activities.

I5630 Beverage serving activities.

N771 Renting and leasing of motor vehicles.

N7721 Renting and leasing of recreational and sports goods.

N791 Travel agency and tour operator activities, also ‘mainly tourism’.

N7990 Other reservation service and related activities.

12. The calculation of the growth rate may differ due to rounding.

13. The data for 2024 in this news release should be considered as provisional and subject to revision.

14. SBS cover only market activities and as such, exclude the public sector and non-profit organisations, except for public corporations classified within the non-financial business economy. Public corporations refer to market-oriented entities that are controlled by the government but operate similarly to private enterprises.

15. Values published in this news release may differ from those in Eurostat’s database (Eurobase) due to differences in size classification, with Eurobase figures based on employment size class only, while this release applies the criteria outlined in Note 9.

16. More information relating to this news release may be accessed at:

17. A detailed news release calendar is available online.

18. References to this news release are to be cited appropriately. For guidance on access and re-use of data please visit our dedicated webpage.

19. For further assistance send your request through our online request form.

L-Istatistika Strutturali tan-Negozju: 2024

- L-intrapriżi mikro, żgħar u medji (SMEs) ikkontribwew 56.1 fil-mija tal-Valur miżjud iġġenerat mill-ekonomija kummerċjali mhux finanzjarja.

- Il-qasam tas-Soluzzjonijiet teknoloġiċi, is-servizzi professjonali u ta’ appoġġ għan-negozju rreġistra l-akbar Valur miżjud fl-2024 (€5.3 biljuni).

- L-SMEs kienu dominanti l-aktar fil-qasam tal-Kostruzzjoni, bis-sehem tagħhom jilħaq is-86.4 fil-mija tal-Valur miżjud iġġenerat minn dan il-qasam.

- L-intrapriżi żgħar bʼkapitalizzazzjoni medja (SMCs) iġġeneraw Valur miżjud ta’ 1.4 biljun, li jiġi daqs 9.4 fil-mija tal-Valur miżjud tal-ekonomija kummerċjali mhux finanzjarja.

L-Istatistika Strutturali tan-Negozju: 2024